What triggered the battery revolution

How Li-ion technology made electric forklifts the only logical choice.

by Max Khabur, Marketing Director Eneroc USA

Ask anyone in material handling why electric forklifts are taking the market share from propane and diesel-powered machines, and you will probably get these answers: E-commerce and narrow aisles in warehouses; emissions regulations and fuel cost. They are not wrong.

The shift toward electric industrial trucks has been underway for more than two decades. What changed recently, and what most industry commentaries overlook, is the rapid decline of lithium iron phosphate (LFP) battery prices that turned lithium from a premium upgrade for the most demanding applications into the most cost-rational choice in the market. That is what is driving the acceleration. And it deserves a closer look.

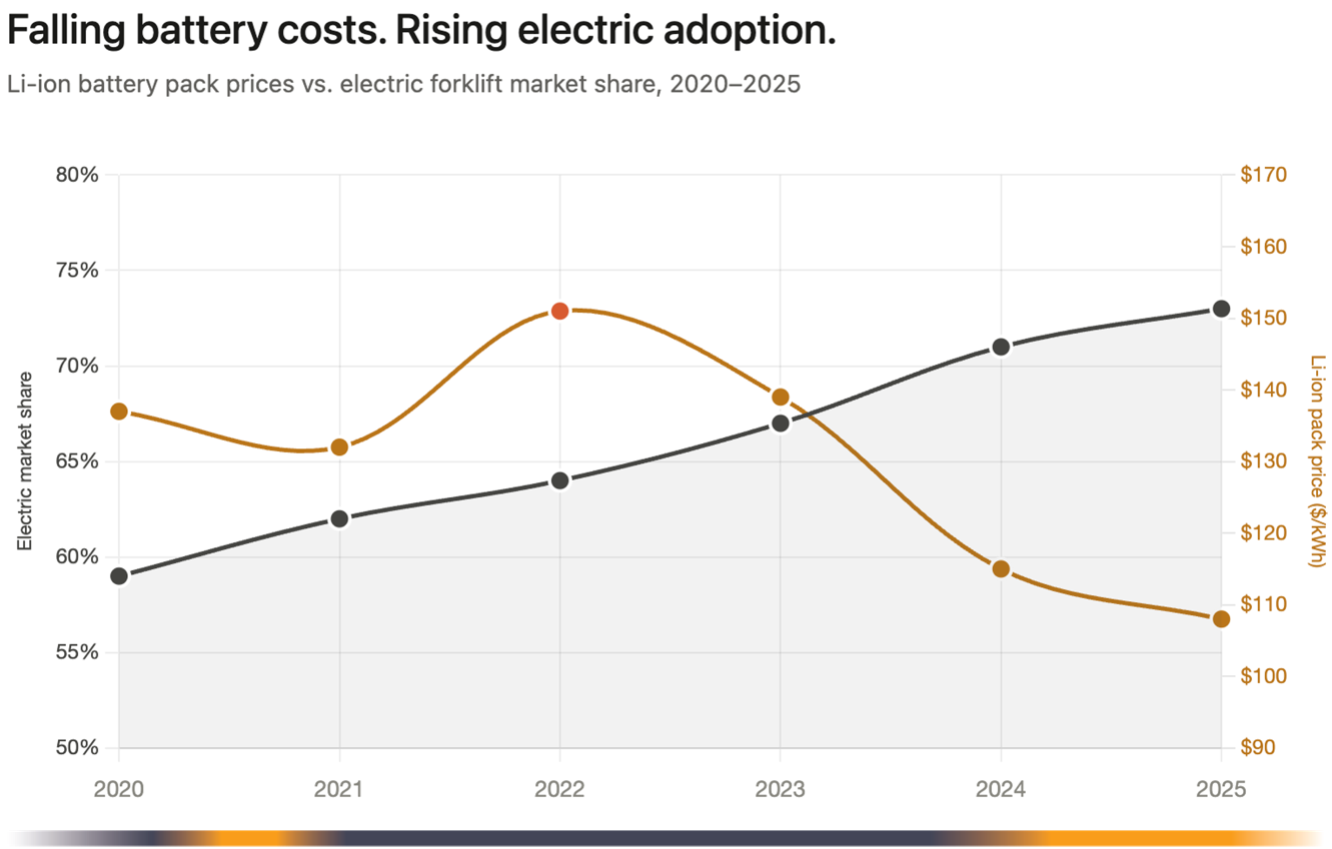

Electric forklift share of total market (%, left axis); Industrial Truck Association (ITA)

Li-ion battery price, pack level ($/kWh, right axis); BloombergNEF

By 2020, electric forklifts already outnumbered internal combustion engine-powered (ICE) shipments globally. In 2024, they accounted for 71 percent of North American retail orders according to the Industrial Truck Association, with Europe exceeding 70 percent. Electric trucks were always the rational indoor default; lead-acid batteries powered them reliably for generations. The trend line was never in doubt.

The question is not whether electric is winning. It is why the pace accelerated so sharply, and why ICE holdouts that resisted for two decades are now converting.

The rise of Class II and Class III

The conventional narrative focuses on the material industry structural shifts, and these are real. The explosion of e-commerce fulfillment has changed what warehouses look like: taller, denser, and more automated.

This market trend has driven strong growth in Class II and Class III trucks; narrow-aisle reach trucks are the fastest-growing electric segment. At MODEX 2026 in Atlanta, one of the panelists of the session hosted by the Advanced Energy Council (AEC) of MHI, addressed this directly:

"We have seen a significant jump in Class II and Class III orders over the last few years. The combination of tighter aisle configurations and operators who simply will not consider anything that produces emissions indoors has made lithium-powered electrical products the default spec for every new fulfillment project we quote."

More modern warehouses mean more specialized and efficient electric lift trucks. It does not explain why Class IV and V ICE users, who resisted electrification for decades, are now converting. And it does not explain why lithium is displacing lead-acid within the electric segment at a rate that is rewriting the battery market. For that, we need to look at what happened to the price of LFP cells.

Price collapse changes everything

LFP is not a new battery chemistry, discovered in the 1980s. But what has happened to its cost over the past five years is without precedent in the battery industry. According to BloombergNEF, Li-ion battery pack prices averaged $137 per kilowatt-hour in 2020, following a long decline from almost $1,000 in the early 2000s as manufacturing volumes grew.

In 2022, prices briefly spiked to $151 per kilowatt-hour, the first-ever annual rise so far, driven by a spike in demand for lithium carbonate. Then the floor gave way.

By 2024, pack prices had fallen to $115 per kilowatt-hour globally, the largest single-year drop since 2017, down 20 percent, and as low as $84 per kilowatt-hour in China. By 2025, the global average reached $108 per kilowatt-hour and is still falling.

This was a structural repricing event, driven by massive battery manufacturing (over)capacity and intense competition among the leaders: CATL, BYD, LG, Gotion, and CALB, the world's dominant lithium battery cell producers. The market responded immediately: Li-ion forklift models expanded 41 percent as cell prices crossed below $90 per kilowatt-hour. In 2024 alone, the Li-ion forklift segment grew more than 10 percent while ICE variants declined one percent and lead-acid-powered models fell seven percent.

Interact Analysis projects lithium will surpass lead-acid in market share within the electric segment around 2026, and that 81 percent of all new electric forklifts shipped globally will carry lithium batteries by 2034. The technology had long since proven its thermal stability, cycle life and safety credentials. What was missing was the price.

Price objection is over

For years, the counterargument to lithium adoption was simple: the upfront cost, typically two to three times that of a conventional lead-acid battery, was a hard stop for capital budgets, regardless of the lower total cost of ownership over a few years. That has changed.

"LFP lithium batteries are nearly at price parity with traditional lead acid in the retail market. When a fleet manager is comparing an ENEROC USA lithium battery against a traditional lead-acid battery, the upfront numbers are now very close. Add in that LFP lithium delivers higher performance from day one, offers a much longer useful life per battery and a longer warranty, the conversation has completely changed. We are still lowering the TCO overall, but now the acquisition price is much lower, too," says Mark D'Amato, vice president of sales at ENEROC USA.

An LFP battery is about 40 percent lower in total cost of ownership than lead-acid in multi-shift power-hungry operations, with positive ROI typically within 36 months and documented fleet savings exceeding $120,000 per ten-truck fleet over five years.

In the context of today’s market prices, this new price parity can be illustrated with an example of a popular forklift battery. Based on a recent price survey, a 48V, 1000Ah capacity model made by a top manufacturer using lead-acid chemistry would cost around $12,000 retail, while its lithium LFP counterpart with similar specifications would sell for $14,000 to $15,000. It is important to note that a similar nickel-manganese-cobalt (NMC) lithium battery can be three times more expensive than a lead-acid battery, and is likely to stay a niche product.

ICE frontier is opening up

As recently as the 2000s, lead-acid batteries couldn't seriously challenge ICE in the heaviest applications. The lift truck electrical systems were inferior as compared to today’s models, and they suffered limitations based on the lead-acid battery technology: strict charging limits, memory effect and voltage drops during discharge, especially at low or freezing temperatures. Li-ion technology solved these problems. Its flat discharge curve means a truck at 80 percent depth of discharge (DOD) lifts and moves as fast as one at 20 percent DOD, resulting in less truck component wear.

Lithium batteries have much higher energy density and can pack much more power into the same-sized battery compartment. Starting in 2024, one after the other, forklift manufacturers introduced heavy electric forklifts with lifting capacity exceeding 20.000 pounds, describing them as “lithium-first” to underline the new generation of electric motive power, replacing propane and diesel for good.

The default has changed

Calling forklift electrification a trend is now outdated. Lead-acid powered electric forklifts for more than a century. For the past decade, lithium was the best technology at a premium price. For the past two years, it has been the best technology at a competitive price. That is the definition of a new default.

The battery revolution in material handling did not begin with a regulation or an e-commerce boom. It began when the most competitive manufacturers in the global battery industry drove LFP prices below the threshold where any other answer stopped making economic sense.

###

Editor’s note: Max Khabur is a director of marketing at Eneroc USA, one of the world's leading manufacturers of industrial lithium batteries. Formerly, Max led marketing at Bluwater and OneCharge Lithium Batteries, and was elected Chairman of the Advanced Energy Council, representing a group of companies - members of the Materials Handling Industry Association (MHI.org).

Data sources: Industrial Truck Association (ITA), BloombergNEF, Interact Analysis, AEC/MHI MODEX 2026 seminar.

PRO CONTRACTOR RENTALS MAGAZINE

Pro Contractor Rentals provides information of value to rental centers who focus time, resources and attention on meeting the demands of construction contractors and other equipment rental customers.